Patterns of Disruption

Observed Lessons from Historical Paradigm Shifts

When a technology platform shifts, who wins?

AI’s inexorable progress has left little doubt that the next, long-awaited paradigm shift is finally here. In contrast to preceding hype cycles, AI is already driving substantive productivity gains. According to CG&C, an outplacement firm, more than 4,600 of their candidates were displaced by AI. The number may seem meager, but it represents a myopic view of what’s happening more broadly.

In ServiceNow’s most recent earnings call, Bill McDermott exemplified the willingness to embrace and pay for AI across the enterprise:

“When you have that C-level executive meeting, they really get it now. And with regard to Gen AI, the momentum is outstanding. As I said, that SKU has outsold any other new introduction we put into the marketplace. So, there's a real appetite to invest in Gen AI, and there's no price sensitivity around it because the business cases are so unbelievable. I mean, if you're improving productivity, 40%, 50%, it just sells itself.” - Bill McDermott

Despite consensus around the technology, a fundamental question remains: Who is at risk, and where will value accrue? Answers to this question are far more controversial…

AI’s Effect on Vertical SaaS

Incumbents vs. Startups

Do open or closed source models win out, which applications are the most interesting to invest in, and are incumbents at risk? Untangling these questions as investors and entrepreneurs is a challenge. And the imperceptible speed at which GenAI technology is advancing compounds it.

In thinking about where I stood with respect to such arguments, I’m reminded of a quote:

“History doesn’t repeat, but it does rhyme.” - Mark Twain

When discussing the future of AI and its respective opportunities, references to historical paradigm shifts are rarely made. In hopes of identifying patterns and lessons learned that may apply to what we’re experiencing today, I chose to explore them. What follows is a series of observations from paradigm shifts that have taken place over the past 40 years. We will explore how startups have historically leveraged platform shifts to their advantage, common mistakes investors make, and evaluate how AI compares.

The Modes of Disruption

From unnetworked applications to the Internet, the mainframe to PCs, on-premise software to cloud, or desktop to mobile, each paradigm shift that resulted in startups displacing incumbents possessed one or more of the following characteristics: A new distribution channel, a shift in business model, and/or a new product architecture. These patterns enabled entrants to be overlooked and eventually achieve market leadership over their respective category incumbent. They provide insight into how AI startups may fare if competing in established markets with incumbents.

1. Distribution

Each platform shift mentioned above provided a new means to distribute technology in an unprecedented way. Leveraging nascent distribution channels provides opportunities for entrants because:

The distribution channel is small and uninteresting at first. Because the technology may only be adopted by a small group of people or organizations, incumbents operate with normalcy bias and tend to dismiss its potential.

(Internet) - “By 2005 or so, it will become clear that the Internet’s impact on the economy has been no greater than the fax machine’s.” - Paul Krugman

(Cloud) - “No one is making money in the cloud.” - Steve Ballmer

(PCs) - “There is no reason for any individual to have a computer in their home.” - Ken Olsen

Skepticism and downright dismissal are common when platforms shift.Incumbents rely on distribution channels that predate the paradigm shift. Go-to-market teams are oriented around already-established channels that produce revenue. GTM re-orientation is a significant undertaking and is difficult to justify when the distribution opportunity appears small.

Perhaps most importantly, new distribution channels enable new segments of customers to be reached by startups, avoiding initial direct competition. Incumbents are slow to see and respond to the threat because they’re not losing customers to the entrants. More on this later.

2. Business Model

Much of an organization is architected around a company’s business model. Changing business models often means rearchitecting an organization. Saas-era incumbents are a canonical example of business model disruption. Incumbents faced an issue if they were to adopt the then-new subscription model, given that it would cannibalize existing contracts/revenue streams. In addition, sales organizations would require restructuring, comp models would need to be retooled, etc. Other paradigm shifts follow a similar pattern, such as PCs utilizing high-volume, low-margin production to unseat mainframe incumbents. Or the dilemma faced by Yahoo with the shift to Mobile:

“Mobile really created an innovator's dilemma with users at Yahoo. For example, we knew that our users wanted mobile, but every time we sent a user from the desktop to the mobile to check Yahoo Mail, we knew that we were getting pennies on the dollar.” - Ramy Adeeb, Founder of 1984 Ventures and former VP of Product at Yahoo:

If a business model cannibalizes existing lines of business or makes a business unit less profitable, the inertia for the incumbent to react and match the entrant increases.

3. Product Architecture

The last disruptive force that commonly exists across paradigm shifts is when the shift necessitates a new product architecture. The shift to cloud is another prime example here. Incumbents not only had to overhaul their business model and sales organizations but would also be tasked with re-engineering their product to a cloud implementation of the legacy product. In addition, product development practices for continuously deploying software updates would have to be instantiated. Again, this is challenging if current customers aren’t demanding it, and the opportunity appears to be small.

These modes enabled startups to gain leverage and eventually displace competition in their respective category. Despite this, there is often a misunderstanding of how startups leveraging these forces displaced their respective competition. Rather than competing directly, most took a circuitous path and focused on a customer segment that is underserved or not served at all by their competition.

Competing with Non-Consumption

In the shift from on-premise to cloud software, most of the biggest winners at the application layer have been cloud implementations of familiar, on-premise products, such as NetSuite vs. SAP, Salesforce vs. Siebel, and Figma vs. Adobe, etc.

If you asked the founders at the time when they founded their business, most would see it as inevitable that cloud software would displace their on-premise mirrored image.

“This is the end of software. The business model of software is dead. Siebel is the last large software company that will be built” - Marc Benioff

Although Salesforce and others saw this as an inevitability, most cloud companies didn’t choose to compete directly with their on-premise competition until years after the product was launched. Instead, they leveraged the disruptive forces mentioned above to serve customers who could not adopt a solution (primarily tapping into SMB and mid-market segments in the shift to cloud software). These segments couldn’t afford to purchase and provision on-premise servers to run Siebel, PeopleSoft, etc., so they were left without a solution.

This gap in the market enabled Salesforce and others to gain a foothold in each respective market, reach product maturity, and gather resources before returning to compete with the once-upon-a-time market leader. In the case of Salesforce, it wasn’t until 2004/2005 that they provided an enterprise offering.

PCs vs mainframes follows a similar story. Steve Jobs saw PCs as an inevitability in a business setting but chose to focus on a customer segment that couldn’t afford a solution: Consumers. PCs would primarily service consumers until the hardware and software ecosystem reached maturity and eventually displaced mainframe incumbents. This journey was a decade-long undertaking, though. The Apple I and II were released in 1976 and 1977, respectively, but it wasn’t until the late 1980s/early 1990s that PCs became ubiquitous in business settings.

The pattern here is that companies that leverage the power that comes with technology underpinning a platform shift generally find footholds in the pockets of customers who are underserved or not served at all by technology. The paradigm shift itself enables these customers to be reached for the first time (think Salesforce serving SMBs) or a new market to form altogether (i.e. internet search).

Focusing on these groups of customers enables startups to build under the cover of time and market uncertainty to gain a foothold in the market and gather resources to compete with established incumbents. Incumbents tend to dismiss the opportunity because they’re not losing customers to entrants. By the time they realize the threat, it’s often too late, as was the case for Siebel. The company tried to launch a cloud version of its product in 2004/2005 and was ultimately acquired in 2006 for less than 10% of its peak enterprise value.

Fortunately, numerous markets still exist that have lagged behind technology adoption and are in the infancy of digital transformation. With AI as a catalyst, we may see technology finally start to penetrate these industries in unprecedented ways, such as we’re already seeing in legal, healthcare, and logistics to name just a few.

Muti-Decade Long Cycle

Much of the focus thus far has been on how winners emerged from categories with existing incumbents. Paradigm shifts also create new markets, though. Those absent of competition altogether. And history shows us that markets that are created from the shift itself tend to be the most fertile for startups.

We as founders and investors naturally get excited and rush to create and fund companies where we think there’s opportunity. If we can’t find fertile ground to start a company, we start one anyway. If we can’t find reasonably priced companies that we have conviction can build enduring companies with durable revenue, history shows us that we invest anyway. This was the case during the dot-com bubble, where more than 7000 businesses failed, and more than $1T+ in assets were lost.

It’s essential to keep in mind that this is a long game. FOMO is natural, but we will still be investing in AI 10-15 years from now, the same way that we’re still founding and investing in cloud businesses more than 25 years after the founding of Salesforce. Participating for the sake of participating begets negative consequences.

Brad Gerstner shared a story on Samir Kaji’s podcast highlighting a lesson learned from the internet era that encapsulates this point well:

(paraphrased for brevity)

In 1997,1998 every venture capital firm knew that the internet was going to be huge and that search was going to be a big and important business in that mix. But who? We know that the 800 lb Gorilla was Yahoo and that they were on top of everything. AOL was also huge. But remember all of the other contenders? Infoseek, Excite, Go, Ask, Lycos. At least 20 of them.

There was a bidding war for the acquisition of Lycos. It was a tectonic battle that David Weatherall would eventually win. He was on the cover of Time Magazine, etc. 2 years after, he was bankrupt.

Was he right that the internet was going to be big? Yes.

Was he right that search was going to be important? Yes.But he picked the wrong horse.

He could’ve waited until 2003 2004. Hell, he could’ve bought Google in the IPO and captured 95% of all of the upside in internet search.-Brad Gerstner

A similar story is observed in cloud security. Companies such as Evident and Redlock were both ultimately acquired by Palo Alto Networks, but both were likely a turn too early to accrue the value that the category would ultimately create. That prize now goes to companies like Wiz, Lacework, and Orca.

This is not to say that the companies we’re seeing in AI today won’t accrue long-term value because some of them certainly will. The point is that there’s a natural inclination for investors and founders to be driven by FOMO, which can lead to irrational decision-making.

“The risk/reward of Anointing someone the winner today and paying the winner valuation today, prior to seeing the durability of revenue or without that visibility, can be dangerous.” - Brad Gerstner

If AI is as big as most claim it to be, founders will still be starting businesses, and investors will be funding them 10-15 years from now. The seeds that create durable value are sown throughout the entirety of the cycle, not just in the first 12 to 24 months.

How Does AI Compare?

Rather than hardware laying the foundation for a new distribution channel, AI is the first software-to-software paradigm shift. Contrasting the characteristics we’ve seen startups leverage from past paradigm shifts, it’s difficult to see the same characteristics in today’s shift.

It’s not to say those won’t be coming, though. It’s possible that we see business models shift toward charging for the work, not the software, as coined by Sarah Tavel. Products may also be entirely reimagined to extend beyond chat interfaces. It remains to be seen, and that is up to the founders who are creating the future.

Like preceding paradigm shifts, AI will not be a zero-sum game, though. Although debate persists on who wins in the next round of incumbent vs. startup, it will be the same answer that each paradigm has shown us in the past: Both.

Some incumbent markets and business models are likely to be exposed and go the way of Siebel, DEC, and the other names that don’t sound familiar but were once market leaders in their respective categories. Others will adapt and grow in size. Technology tends to be multiplicative and create entirely new markets, but, as mentioned above, some of these derivative markets may take time to develop.

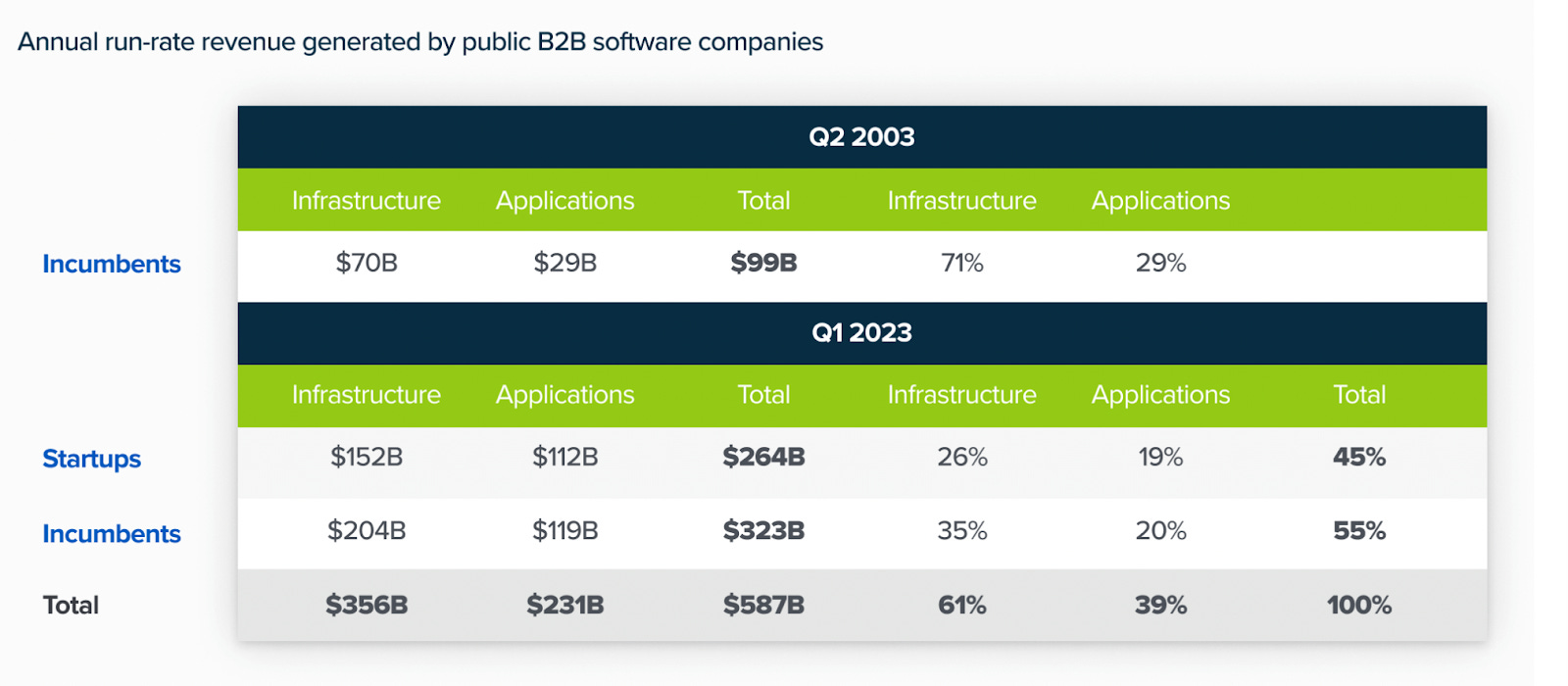

A16z wrote a piece on how this unfolded with the shift to cloud at the application and infrastructure layer.

“Software incumbents have grown from generating $99B to $323B, maintaining 55% of market share. Or, put another way, incumbents have added revenue but lost 45% of the market to new entrants. And 2 decades into SaaS, there’s still plenty of value left to capture—Morgan Stanley recently estimated cloud workloads to be only 29% penetrated in the enterprise”

Only time will tell who wins in the age of AI. If history has taught us anything though, the shift to AI will not be a zero-sum game. We will likely see new startups build generational companies and pockets of incumbents grow even larger.

Founders with high customer centricity and who are focused on solving problems and serving segments where incumbents do not reside are especially ripe during paradigm shifts. Fortunately, numerous markets still exist that have lagged behind technology adoption and are in the infancy of digital transformation. With AI as a catalyst, it’s possible that we will see technology finally start to penetrate these industries in unprecedented ways, such as we’re already seeing in legal, healthcare, and logistics, to name just a few.

If are building an application in one of these spaces, I would love to hear from you - nate[at]newstack.com