The Mechanics of Unbundling Part III - Network Effects Type & Strength

A Deep Dive Into how Horizontal Platforms Truly Become Unbundled.

Welcome Back

If you’re reading Bits & Bytes for the first time, I recommend reading parts I & II before jumping into Part III. If you’re a recurring reader, some quick notes:

Here’s where we’re at in our journey:

- Part I - Carrying Capacity

- Part II - Platform Dimensionality

- Part III - Network Effects Type & Strength

- Part IV - Putting the Pieces Together

TLDR from Parts I & II

In Part I, we built the foundation for understanding how an individual sub-network becomes unbundled from an incumbent horizontal platform. When a platform cannot adequately support the volume of transactions passing through its subnetworks, opportunities present themselves for challengers to build a vertically integrated solution. Our analysis showed that each sub-network possesses a unique carrying capacity - the threshold of transactions that can support through the platform. To understand when networks crumble, and the former participants opt for a vertical solution, we analyzed Craigslist and explained why Craigslist thrives in rural states but falls apart in dense metro areas.

In Part II, we built upon the concept of carrying capacity and expanded our analysis from an individual sub-network to an entire platform. We answered questions such as why eBay opted to acquire StubHub versus compete and why their revenue (larger than all of the vertical competitors combined) is comprised almost entirely of commodity goods. We also explained why we see a few big winners in the unbundling of Craigslist, versus several of equal size. The answer is rooted in the variety and quantity of subnetworks. To better understand variety, we provided characteristics in which verticals distinguish themselves. Understanding the quantity and strength of sub-networks is the topic of Part III.

Is Uber a more attractive and defensible business than DoorDash? Is either of the two more or less vulnerable to facing niche competitors, and who is the most likely to produce economic profits relative to Airbnb?

As discussed previously, competition and the likelihood that an incumbent responds to a vertical threat largely depends on how heterogenous the use cases/types of suppliers the platform supports. The analysis involving the type and strength of its network effects is equally as important, though.

All platforms exhibit some form of network effects, where the value of the product/platform increases the more participants that join it. Not all network effects are created equally, though. The characteristics of platforms and marketplaces leave some more defensible and less likely to face competition.

Types of Network Effects

Platforms and marketplaces fall into one of two camps. They are either global or local in nature.

Local network effect - A network whose suppliers only derive value from demand localized to a specific geography. Doordash, Craigslist, Tinder, Fixer, etc.

Global network effect - A network whose suppliers find value from demand independent of location. eBay, Airbnb, Reddit, Goat, Poshmark, etc.

*Note that this is putting aside the nuances like direct, indirect, etc. More reading on that can be found on NFX.

The level of competition and the relative financial benefit of being larger than its competitors a business will receive starts with this broad classification. In addition, the potential strength of its network effects, or the measure of additional value the network receives from each additional participant, determines the threshold challengers must meet to be competitive.

Businesses that exhibit local network effects are more susceptible to challengers due to the sheer quantity of networks that they must defend. Each network is unique and doesn’t benefit from the demand or supply-side advantages of the other geographies. For example, drivers on Uber’s platform in Miami are not concerned about the riders in Chicago. The value is inherently localized and isolated from one another.

In contrast, supply and demand create a symbiotic relationship for businesses that exhibit global network effects, independent of location. This geo-independent relationship creates a denser network, as the supply and demand are not clustered and isolated but rather compound on one another. Even in the case of Airbnb, hosts are concerned not only about the density of listings in their local geographic area but also about the awareness of the marketplace in popular travel destinations as a whole. Optionality increases the number of travelers attracted to the platform, making Airbnb even more attractive for hosts.

Mapping out the network effects of each respective business looks something like this:

Businesses that exhibit global network effects, like Airbnb, have higher fixed costs on the supply side. This advantage is beneficial because these platforms can spread the overhead across an entire network, not a specific locale. Any competitor to Airbnb would have to enter on a global scale, and the few that do compete, Expedia and Booking.com highlight the importance of a global footprint.

An excerpt from The Platform Delusion by Jonathan Knee:

Although both are global, Expedia acquired a portfolio of locally focused brands while Booking uses its core brand globally. As Expedia belatedly realized that the ability to attract international demand from vacationers for a local listing placed on a service unknown outside of its home country is limited. After five years, Expedia retired its HomeAway brand in the US and established Vrbo as its global brand in 2020, although it still maintains multiple local brands like Abritel in France, Stayz in Australia, Bookabach in New Zealand, and FeWo-direkt in Germany. Despite spending $3.9B for the HomeAway portfolio, Expedia generates less than half of the revenue of Booking’s organically generated business.

For businesses with local network effects, competitors to Uber, Fixer, Doordash, etc., need not be global to compete. However, due to the lower barrier to entry, we see several competitors that have emerged in ride-sharing and delivery, each with a specific demographic in mind to serve, many carving out their niche geographically.

Network Effect Strength

The type of network effect broadly describes how likely a platform is to see competition in its market, but it lacks any further fidelity. The intensity of competition is also variable across businesses that exhibit each type of network effect. Food delivery and ride share are both categorized as local network effect categories of businesses. Yet, I would argue that the barriers to entry in rideshare are higher, and the advantage of scale is stronger than that of food delivery.

To complete the picture of how intense the competition will be for both local and global network effects businesses, we must understand how strong of a network effect the incumbent possesses and how likely it is to ward off competitors. I.e., what minimally viable service or product must a competitor offer to breed liquidity? The lower this threshold is, the lower the barrier to entry for potential competitors.

Determining this threshold is more straightforward in some cases than others.

For ride-share businesses, consumer considerations are dominated by price and the ability to quickly attain a ride (Uber estimates this to be 3-5 minutes). Therefore, bolstering the supply side to a level that delivers rides faster is unnecessary and doesn’t provide additional value to the user.

Andrew Chen - Former Head of Growth at Uber:

“Eventually, the value of the network plateaus — there’s a diminishing return to having more density of drivers; it doesn’t matter if you can get four minutes versus two minutes versus having a driver instantly outside. In fact, it’s kind of inconvenient, since you need a little time to get your keys and jump out the door to meet your driver.”

*Excerpt from the Cold Start Problem

In addition, because the supply side in ride-share is homogenous, consumers are less loyal as rides are seen as indistinguishable from one another. The interchangeability between drivers among riders and vice versa ultimately means that likelihood a platform can keep both sides captive is lower.

According to the rideshareguy, “83.5% of drivers surveyed work for multiple rideshare apps. For consumers, checking multiple rideshare apps is a common ritual before booking a trip.

The lower barriers reinforce the number of companies we see competing. Any service that can attract enough drivers to provide a comparable level of service will be competitive in the market. The result is competitive threats at a regional and local level vying for market share.

This graphic only mentions a handful of the total number of competitors. It doesn’t point out how services like HopSkipDrive (children), Gett (business travel), Wingz (airport rides), etc., cater to specific profiles of riders.

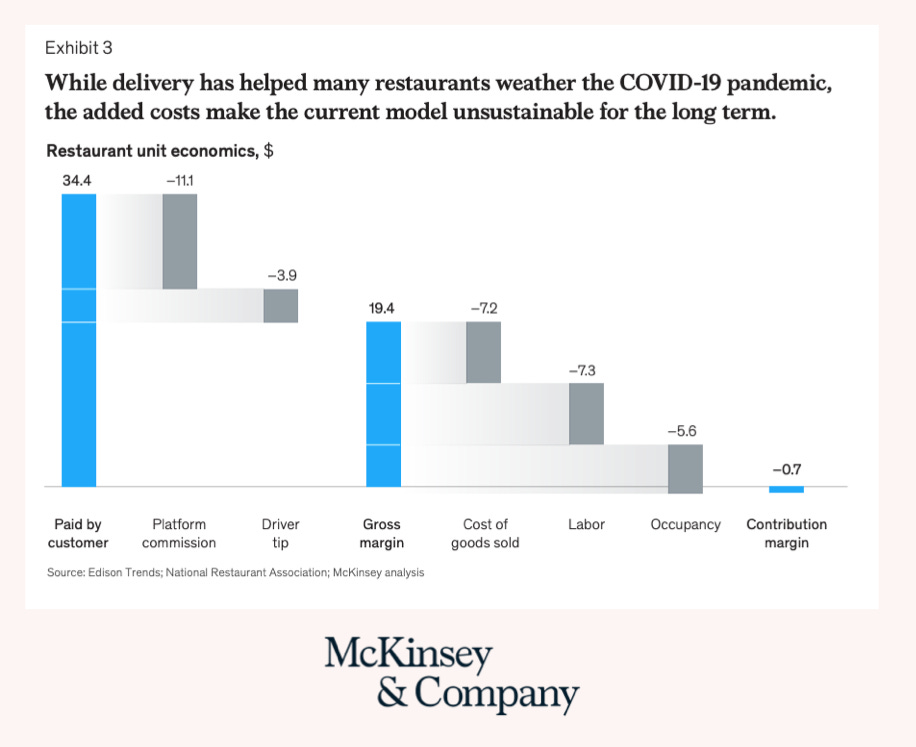

For another category of businesses that exhibit local network effects, food delivery, the threshold to provide a comparable alternative is even lower, and the market has even lower break-even market shares. In short, the market is even more competitive than ride-sharing with tighter margins.

Because consumers are less forgiving about the arrival of their food compared to a 3-5 minute delivery for a car, food delivery services require less density on the supply side of drivers. Because customer captivity is more challenging, we’ve seen food delivery services such as GrubHub offer GrubHub+ (unlimited free delivery), and Uber offer UberPass (discounts across services). DoorDash has gone a different route choosing to hold the supply side captive instead of the demand. By providing restaurant software, Doordash hopes it can be the sole meal delivery provider for the restaurants it partners with, preventing multi-tenanting.

For businesses that exhibit global network effects, like Airbnb, the threshold of a viable alternative is more challenging to put our finger on. Still, we can both qualitatively reason why this threshold is higher and look to their performance in the market to help us quantify.

Airbnb’s advantage is rooted in the fact that both sides are distinguishable from alternatives on the platform for both the supply and demand sides, and both sides must opt into the transaction. In addition, consumers have a broader range of preferences regarding where they’re staying; therefore, more supply further increases the value on the platform rather than plateauing.

Comparing businesses like DoorDash and Uber, which we’re claiming to have a diminishing return on each incremental unit of supply past a certain threshold, with a business like Airbnb, which we’re positing has a much higher threshold, the benefits from this discrepancy in the public markets for Airbnb is clear. Airbnb’s gross margin, ~80%, resembles that of a SaaS company and is nearly 2x compared to Uber’s 46%. In addition, Airbnb is profitable, posting a net 18% profit margin, while Uber, Lyft, and other delivery businesses are still hemorrhaging money as much of the revenue is reinvested into customer acquisition. Public market investors have also rewarded this perceived moat with Airbnb boasting a $68B valuation and a 58 P/E ratio.

Putting the Pieces Together

Not all network effects are created equal. The fragmentation and relative strength depend on:

Whether the network effect is local or global.

The threshold to provide a viable alternative. Does the network get stronger with each incremental participant, or is there a threshold in which the maximum value is delivered to both sides of the marketplace?

Analyzing the latter is more subjective, and we could write an entire article series at to how better assess the strengths of a platform’s network effect.

What we’ve shown, though, is that platforms that are localized and have low barriers of entry to provide a competitive service (through the strength of their network effect) will face stronger competition. In addition, the financial benefit of being larger than the competition is also less appealing than their global counterparts. We see these phenomena play out in the food delivery and ride share wars compared to the competitive advantages that Airbnb enjoys.

Combing previous analysis of platform heterogeneity from Part II with our analysis of network effects will complete the basic framework for understanding how likely a platform is to face vertical competition.

In the capstone piece of this series, we will sum each of the principles we’ve discussed into a holistic framework to make more accurate predictions as to how likely incumbents are to face vertical competition.

Good series so far.

1) The dimensionality is good analysis when the features vary by subnetwork. Definitely lends itself to vertical competition in subnetworks.

2) Network effects are a little more variable based on business I think, as local-based competition is very different for food delivery vs short term rentals. Another network to check out and think about in your analysis is FieldNation, a US-based platform for onsite technicians supporting PC/POS/Cable installs and maintenance. They seem to match high-capacity (invested in their features) while being a single vertical. Their "global" geography provides barriers to entry for local-only competitors.

One other platform is Rover, for pet sitting (they have a nice platform). You would think pet-sitting services are a collection of subnetworks, but building up supply is a barrier to entry and haven't seen an obvious competitor in the overall market , unlike Lyft arising to challenge Uber. Technically, you might say that there should be the potential for a competitor to arise in local markets to combat Rover...just haven't come across one yet.